There are several factors that can contribute to higher mortgage rates, including:

1) Inflation: When the rate of inflation is high, mortgage rates tend to increase as well, because lenders need to compensate for the loss of purchasing power of the dollar.

2) Economic Growth: When the economy is growing at a strong pace, demand for housing and other forms of credit typically increases, which can drive up mortgage rates.

3) Monetary Policy: The Federal Reserve can influence mortgage rates through its monetary policy decisions. If the Fed raises interest rates, for example, mortgage rates will also tend to rise.

4) Risk Premium: Lenders charge higher interest rates on mortgages when the lending environment suggests that repayment may become increasingly difficult and therefore the risk of default is also increasing. This may be due to several factors including the above factors.

Overall, the Fed is trying to slow down the economic growth to combat inflation they themselves caused with poor monetary policy over the past years. By increasing the rate at which banks are able to access money from the Fed as well as one another, this causes mortgage rates to increase to provide investors with the desired rate of return on their investment.

Meanwhile, there are fewer buyers in the secondary market to actually purchase your mortgage after closing as a result of increasing delinquent loans, evaporating savings, increased credit card debt and 401k hardship loans at one of the highest on record. These all cause investors to charge a higher rate in order to access the capital needed to fund your loan.

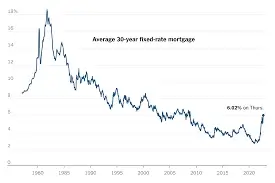

So the above factors ALL contribute to the current state of the real estate and lending environment being very challenging. The good news is that we are still WELL below historical averages for a 30-year fixed rate mortgage. Just because you are no longer to obtain a 3.5% loan for 30 years doesn't mean that a new home isn't in your future.

There are several loan programs that assist with down payments, lower rates and lower payments that may still be better than continuing to rent with no benefit. I also predict that rates will come down towards the second quarter as those investors who aren't currently getting the loan volume required to stay in business will need to be more creative and find ways to reduce the costs of homeownership. This may come in the form of lower rates, lower down payment requirements and/or down payment assistance programs. Rates have been here or higher before.

The market finds a way to support the goal of home ownership and will do so again sooner than later. Please feel free to reach out and discuss your scenario with me and find out if you can take the step into purchasing your first or next home. Looking forward to speaking with you soon, Phil.